Top-Down Budgeting vs Bottom-Up Forecasting: Which Works for Scaling Teams in 2026?

Top-down budgeting vs. bottom-up forecasting: when to use each, key tradeoffs, and how to build accurate, board-ready compensation plans for scaling teams.

Every year, finance teams set a compensation budget, only for HR to discover it doesn’t fully cover what’s needed. This gap points to a bigger issue in how most organizations handle pay budgeting, relying on outdated methods that aren’t equipped to deal with today’s challenges.

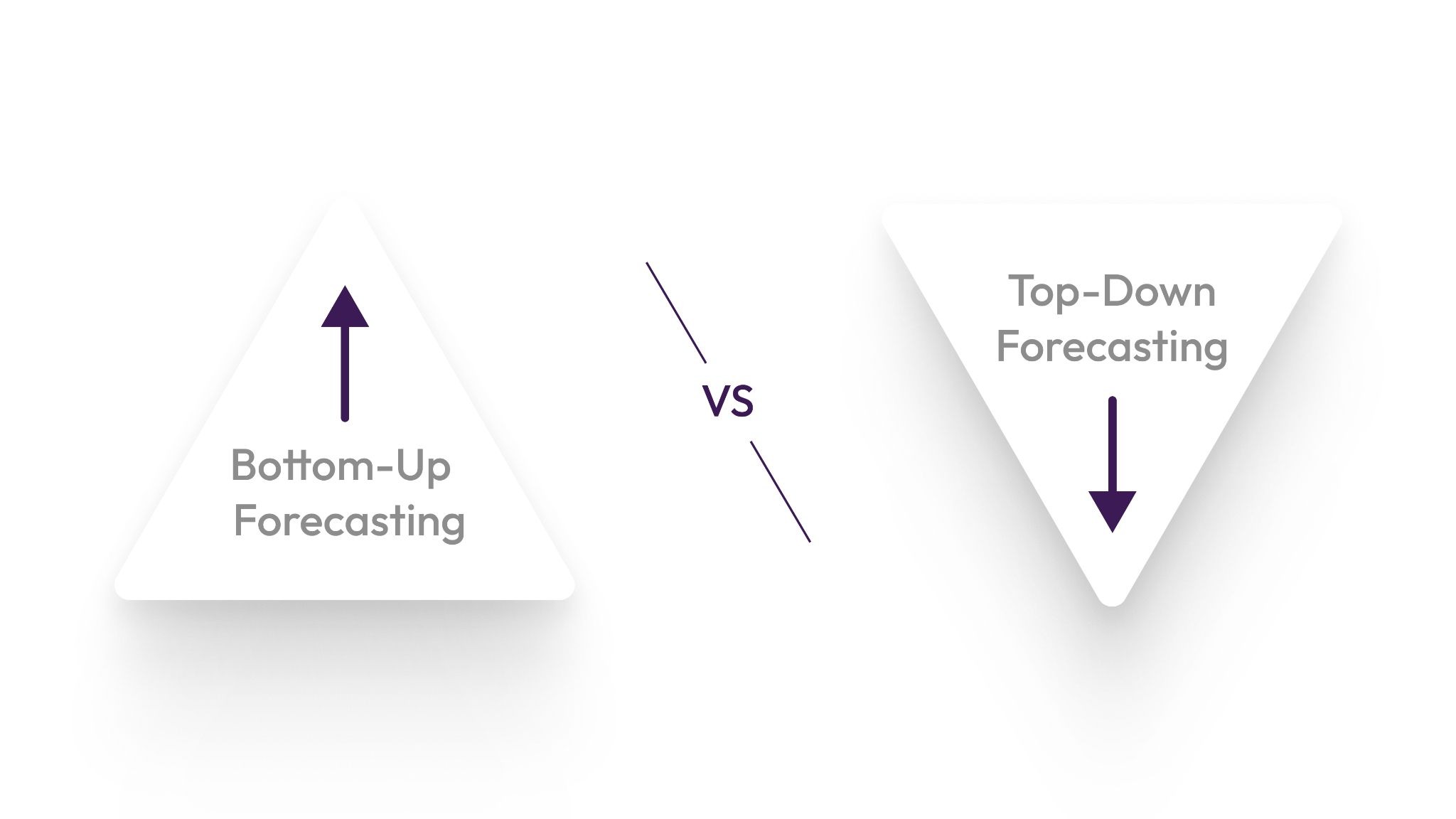

Most companies start with a top-down budgeting model, where leadership applies a percentage increase based on last year’s spend. While this works well in stable situations, it falls short when teams are scaling, restructuring, or facing pay equity adjustments and market shifts.

For instance, Mercer reports a 3.5% average salary increase for 2026, while healthcare benefit costs are expected to rise by 10%. This creates a mismatch that basic percentage-based forecasting can’t address.

That’s where top-down budgeting and bottom-up forecasting come into play. By combining these approaches, teams can create more accurate, adaptable compensation forecasts. In this article, we’ll explore both methods and how to use them effectively to ensure your forecasts align with actual needs.

Key Takeaways

- Top-down budgeting is fast and leadership-friendly, but it often underestimates actual hiring and retention costs at the team level.

- Bottom-up forecasting builds from real role data and gives HR and Finance a shared, defensible number, but it requires more effort and better tooling.

- The best approach for scaling teams is not choosing one model over the other. It is using top-down as a guardrail and bottom-up as the detail layer.

- U.S. salary increase budgets are projected at 3.5% in 2026, making accurate forecasting more critical than ever when every dollar is being scrutinized.

- CandorIQ bridges the HR-Finance gap by turning role-level compensation data into board-ready forecasts, without the spreadsheet chaos.

Top-Down Budgeting: What It Is and When It Actually Works?

Top-down budgeting is the most common way organizations plan compensation. Leadership sets an overall budget based on last year’s spend, expected revenue, and cost targets. That number is then allocated across teams, with managers expected to work within those limits.

The appeal is straightforward. It is fast, easy to communicate, and gives Finance a clear level of control over total spend.

When it actually works:

- Headcount and structure are relatively stable year over year.

- The organization has consistent historical data to anchor decisions.

- Speed matters more than granularity, for example, in early-stage planning cycles.

- Leadership needs a board-ready number before the detailed analysis is complete.

But the model has clear limits. It assumes that next year will look similar to the last, with incremental changes rather than structural shifts. In these cases, a fixed budget can quickly become a constraint rather than a guide.

In contrast, bottom-up forecasting starts from the opposite direction.

The Benefits of Bottom-Up Compensation Forecasting

Instead of setting a budget first, bottom-up approaches build the forecast using actual employee-level data.

Each role, salary, planned hire, promotion, and adjustment is factored in. The total budget is then calculated based on these inputs, rather than assumed upfront.

This approach takes more effort, but it reflects how compensation decisions are actually made.

In practice, teams model:

- current salaries and pay bands

- planned hires and expected start dates

- promotions and internal moves

- retention adjustments or equity corrections

Because the inputs are more detailed, the output tends to be more accurate. It captures where costs are likely to change, instead of smoothing everything into a single percentage increase.

This becomes especially important in environments where change is constant. Growing teams, competitive hiring markets, and ongoing pay adjustments all introduce variability that top-down models struggle to capture.

Also Read: Understanding the Differences Between Salary and Hiring Ranges

For many organizations, the most practical approach is not choosing one model over the other, but combining them.

Top-Down vs Bottom-Up Forecasting: Which Should You Use?

Most teams do not fail because they chose the wrong model. They fail because they rely on one model to do a job it was never designed for.

Here’s a clear comparison between them:

However, most teams are not operating in a single, consistent state. The real challenge is keeping both models aligned as plans change. When compensation data, hiring plans, and budget inputs sit in different systems, that reconciliation becomes manual and inconsistent.

Top-down budgeting answers: How much can we spend? Bottom-up forecasting answers: what will we actually spend, given our plans? So the difficult question is which one to choose and exactly when?

When to Use a Top-Down vs. Bottom-Up Approach

The right approach depends on how stable your environment is, how much visibility you have into upcoming decisions, and how precise your planning needs to be.

The table below breaks down when each approach is more effective, based on real operating conditions:

Also Read: 6 Effective Communication Strategies for Total Rewards

However, most teams struggle with making it work once planning begins. Because in practice, top-down and bottom-up don’t operate in isolation. They need to work together, and more importantly, stay aligned as decisions evolve.

The next section breaks down how to actually implement a budgeting approach that connects both models.

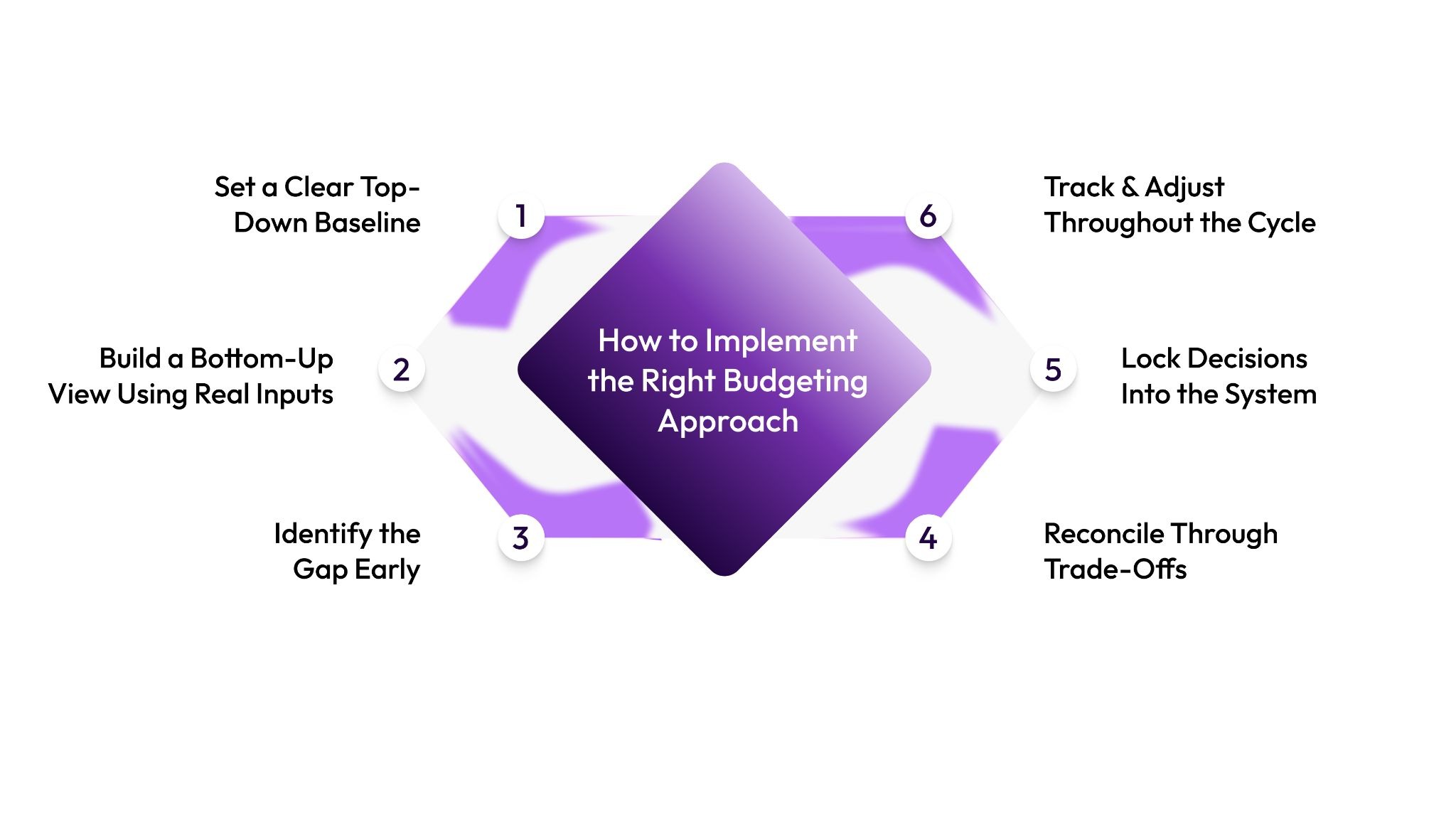

How to Implement the Right Budgeting Approach in 2026 (Step by Step)

Choosing the right model is only part of the problem. Most teams already know they should combine top-down and bottom-up approaches. But, the real challenge is making that work in practice.

The process below focuses on how to actually implement a system that stays aligned as decisions evolve, instead of drifting apart mid-cycle.

Step 1: Set a Clear Top-Down Baseline

Start by establishing a directional budget based on revenue targets, last year’s spend, and cost constraints.

This is not your final answer. It is your starting point.

The goal here is to:

- Align leadership on total spend expectations

- Define guardrails early

- Avoid open-ended planning

Without this step, bottom-up planning can expand quickly without a clear boundary.

Step 2: Build a Bottom-Up View Using Real Inputs

Once the baseline is set, shift focus to what the organization is actually planning to do.

Model:

- Current employee compensation

- Planned hires and timelines

- Promotions and internal moves

- Retention or market adjustments

This is where the plan starts to reflect reality. Instead of assuming a percentage increase, you’re mapping actual decisions to actual costs.

Step 3: Identify the Gap Early

At this stage, the two numbers will rarely match.

That gap is not a problem. It is the point of the process.

Break it down clearly:

- Is hiring driving the increase?

- Are pay adjustments higher than expected?

- Are there structural inequities being corrected?

The earlier this gap is visible, the easier it is to act on.

Step 4: Reconcile Through Trade-Offs

This is where real planning happens.

Instead of forcing everything into the budget or expanding the budget to fit everything, teams need to make explicit trade-offs:

- Adjust hiring timelines

- Phase compensation changes

- Revisit role priorities

- Reallocate budgets across teams

This step turns planning from a calculation into a decision-making process.

Step 5: Lock Decisions Into the System

One of the most common failure points is that agreed decisions don’t carry through to execution.

To avoid this:

- Ensure approved changes are reflected in your planning system

- Reduce manual re-entry across tools

- Document the rationale behind key decisions

If decisions can be easily changed later without context, the planning process loses credibility.

Step 6: Track and Adjust Throughout the Cycle

Planning does not end once the budget is approved.

As the year progresses:

- Hiring timelines shift

- Attrition changes

- New compensation decisions emerge

A working system continuously updates the bottom-up view and compares it against the original top-down guardrails. This keeps the plan grounded in reality, instead of treating it as a static document.

Also Read: Proven Strategies for Compensation Budget Planning

However, when compensation data, hiring plans, and budget tracking live in separate systems, keeping this process aligned becomes manual and error-prone.

.png)

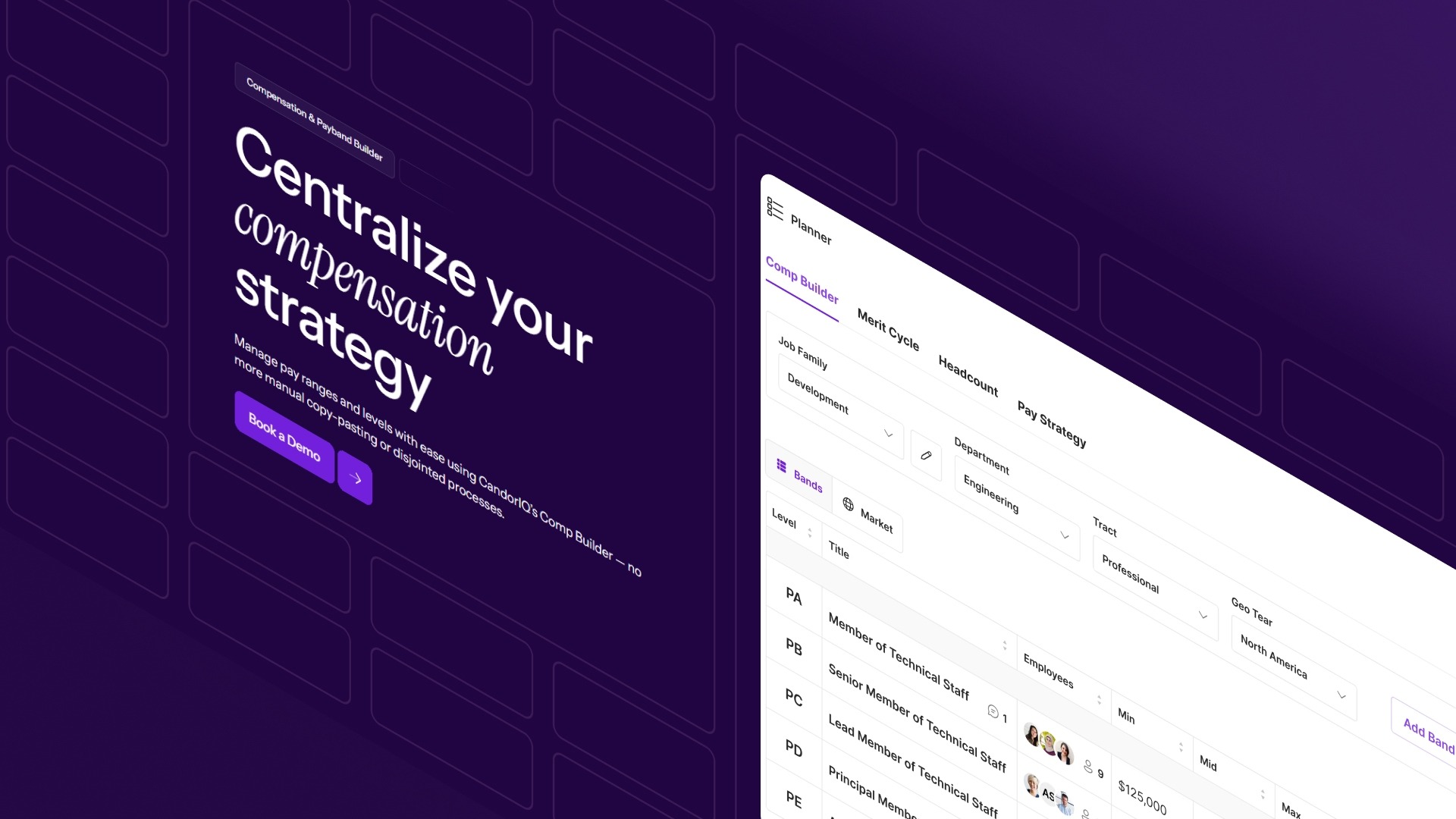

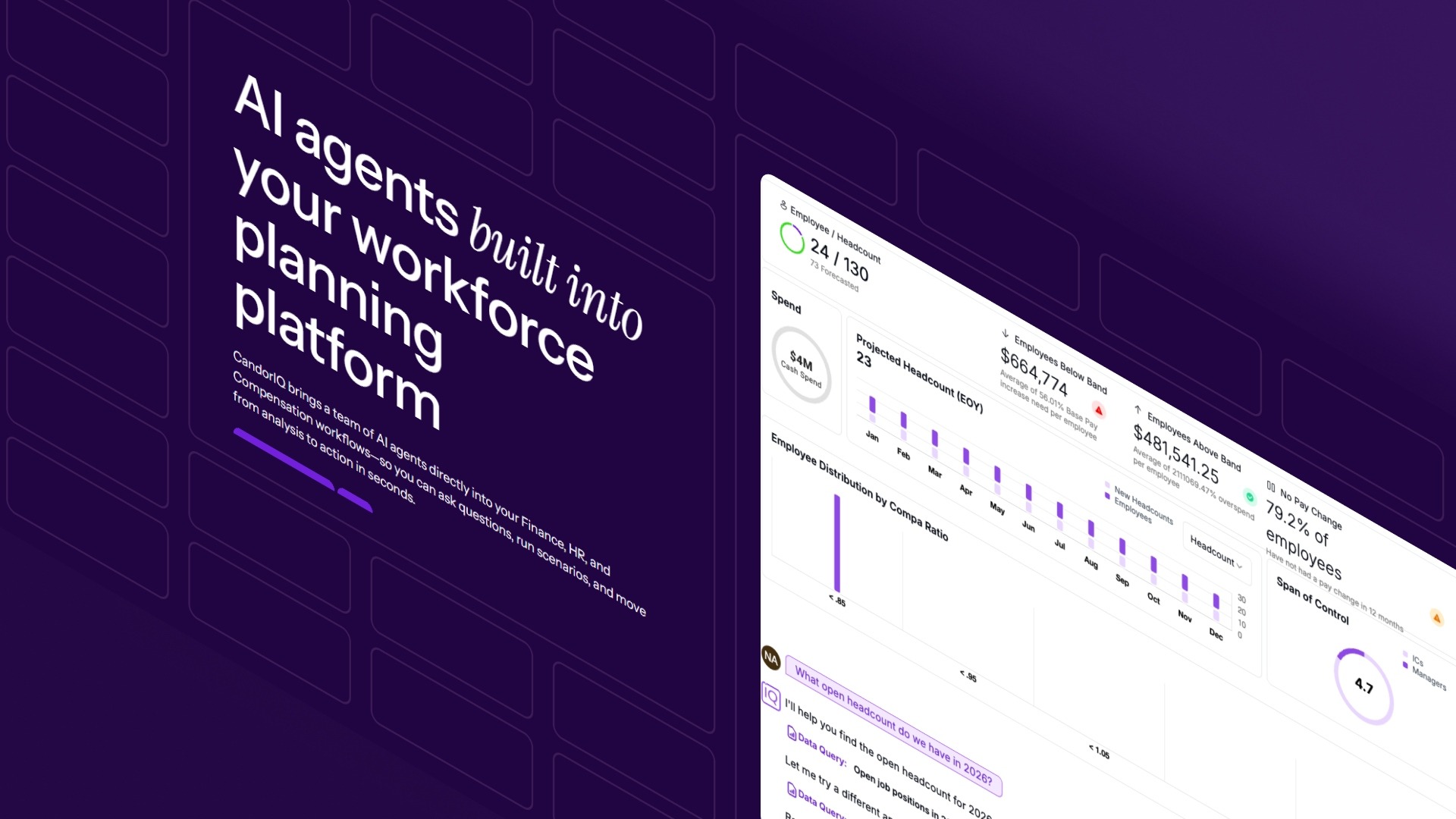

How CandorIQ Helps HR and Finance Build One Unified Forecast

Alt text:How CandorIQ Helps HR and Finance Build One Unified Forecast

By the time you reach execution, the problem is rarely the budgeting model itself. It is the disconnect between systems. That is where most budgeting processes fail, not because the strategy is wrong, but because the infrastructure cannot support it.

CandorIQ is built to solve this exact gap. We bring compensation, headcount planning, and budget tracking into a single system, which helps keep top-down guardrails and bottom-up inputs aligned throughout the cycle. Instead of stitching together spreadsheets and tools, your teams can plan, validate, and execute decisions in one place, with full visibility and control.

Here’s what we offer:

- Compensation & Payband Builder: Define pay bands by role, location, and level, with real-time visibility into pay distribution, so compensation decisions stay consistent and defensible.

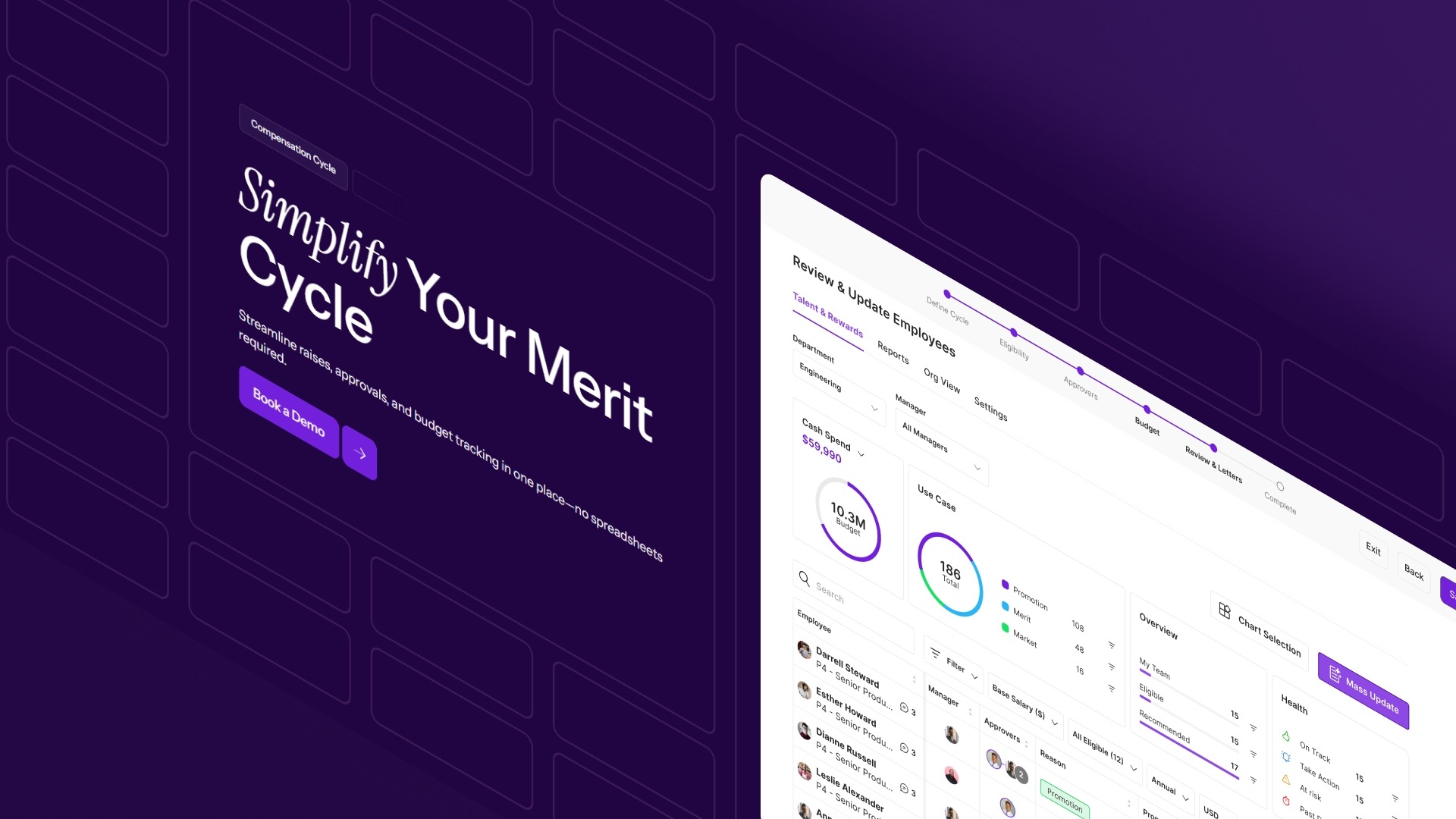

- Compensation Cycle Management: Run merit and bonus cycles with built-in approvals, budget tracking, and rationale logging, so decisions are structured, visible, and easy to track.

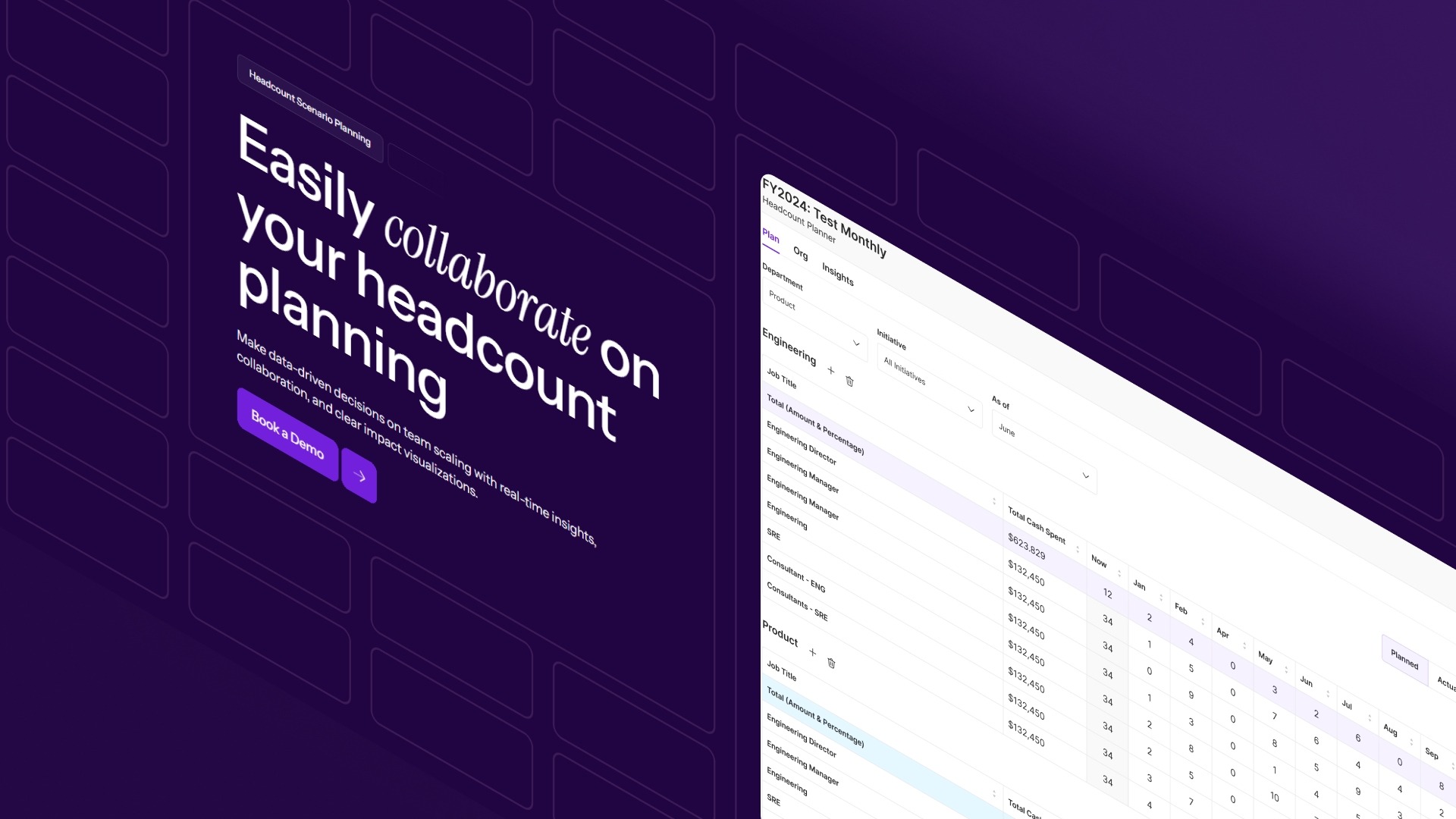

- Headcount Scenario Planning: Model hiring plans and instantly see their budget impact, so teams can evaluate trade-offs before committing.

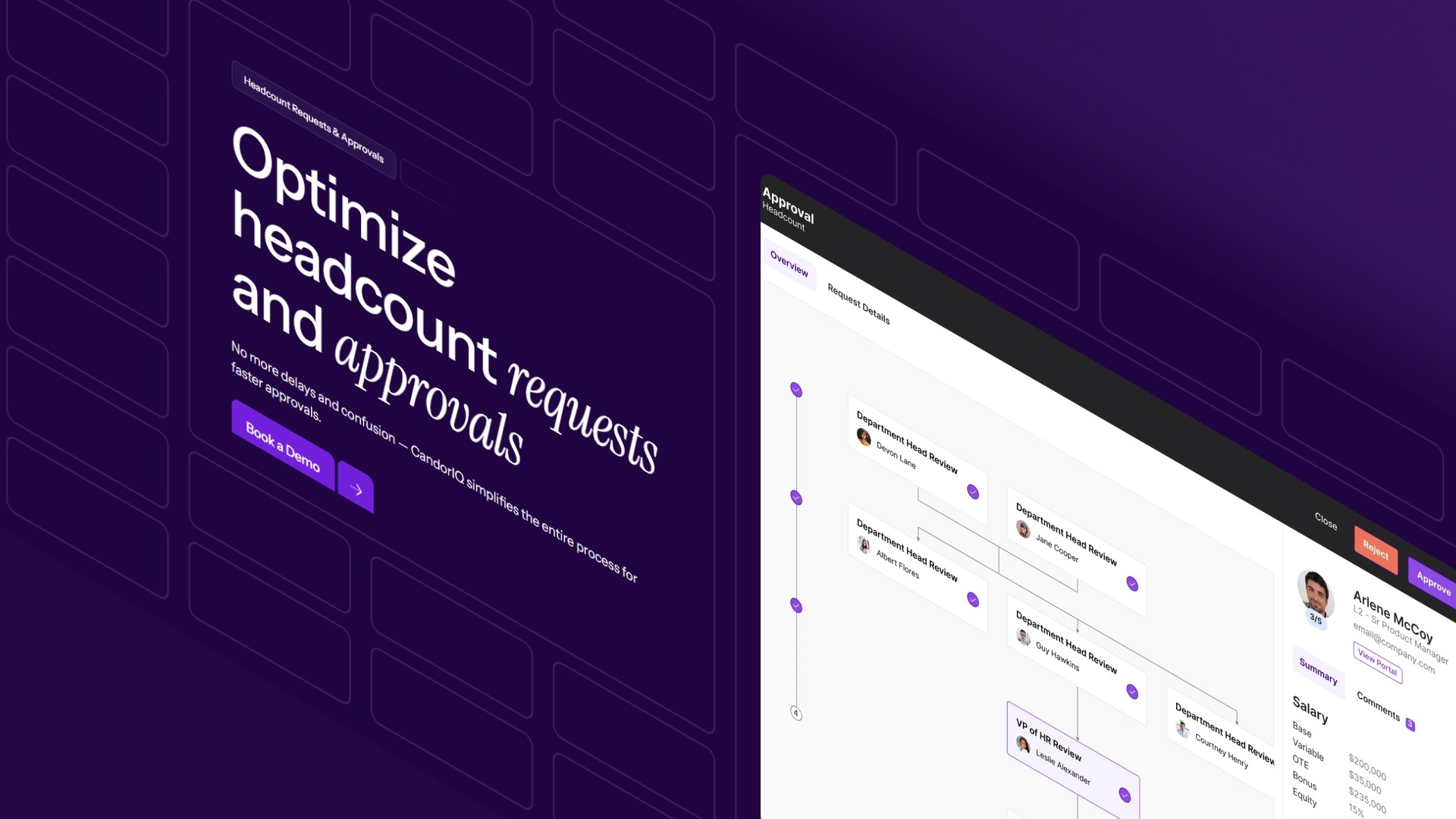

- Headcount Requests & Approvals: Standardize hiring requests with embedded budgets and routing logic, so approvals move faster without losing context.

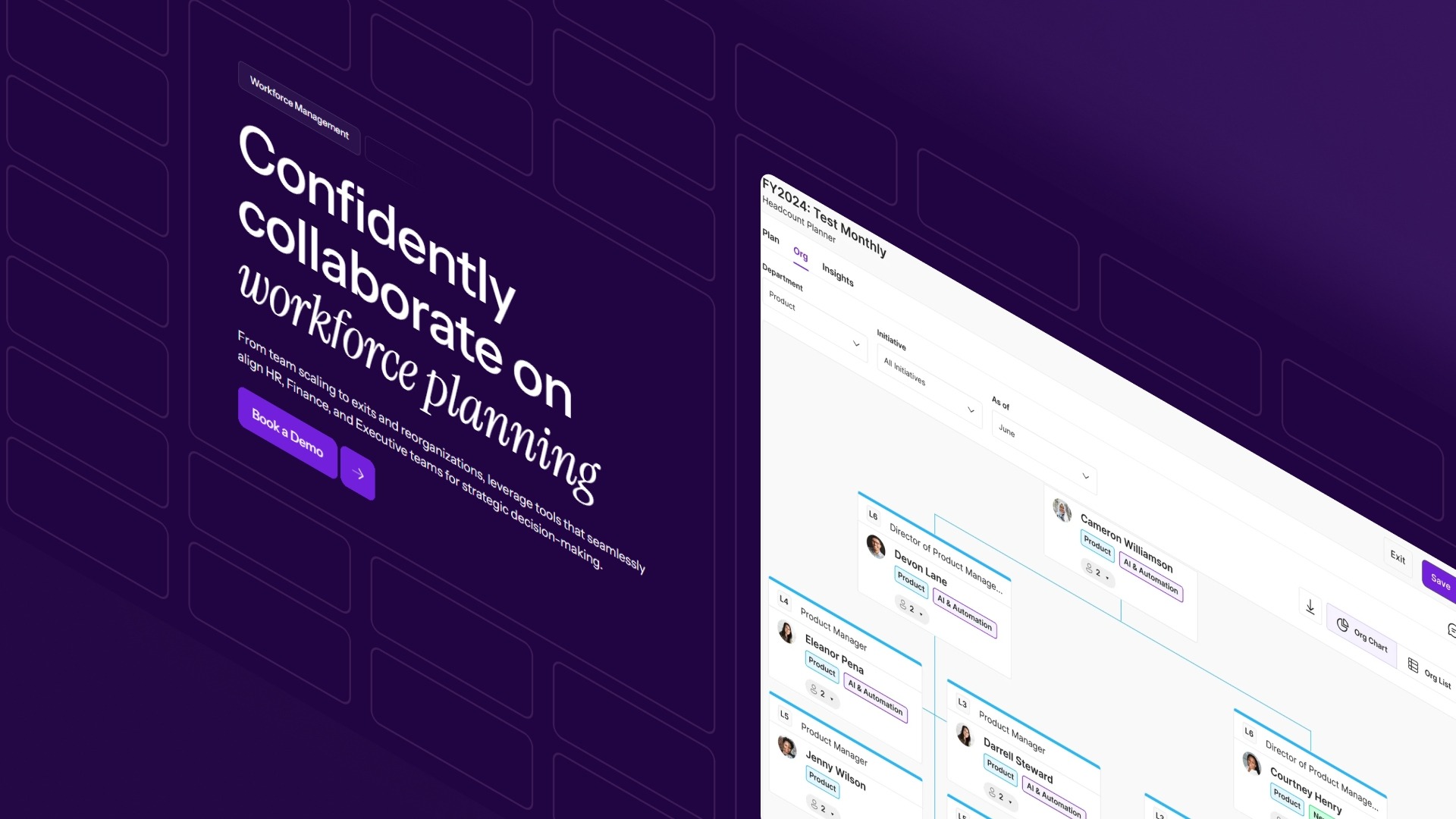

- Workforce Management Dashboards: Track headcount, attrition, and compensation against plan in one view, so HR, Finance, and leadership stay aligned.

- Candidate Offers: Present clear, transparent compensation breakdowns, improving candidate experience, and reducing back-and-forth during hiring.

- AI Agent for Planning Support: Analyze comp gaps, forecast costs, and answer planning questions instantly, reducing manual effort and speeding up decision-making.

With CandorIQ, you will get a planning system where budgets and real decisions stay connected, before, during, and after the cycle.

FAQs

What data is required for accurate compensation budgeting?

At minimum: current employee salaries, pay bands, planned hires, promotion timelines, attrition assumptions, and confirmed budgets. Missing any of these reduces forecast reliability and increases the risk of mid-cycle adjustments.

Is bottom-up forecasting always more accurate than top-down budgeting?

Bottom-up forecasting is generally more accurate because it uses real inputs. However, without constraints, it can overestimate spending. Accuracy comes from combining bottom-up inputs with top-down guardrails—not using either in isolation.

Why do compensation budgets and actuals not match?

The mismatch usually happens because budgets are set using assumptions, while actual spend is driven by real decisions. Without a bottom-up model, hiring delays, pay corrections, and market shifts create gaps that were never accounted for.

What causes compensation forecasts to go over budget mid-year?

The most common reasons are: unplanned promotions, new hire salaries that exceed budget assumptions, off-cycle market adjustments for retention, and benefit cost increases that were not modeled separately. Each of these requires line-item visibility, which a flat top-down percentage does not provide.

Do pay transparency laws affect how I should build my compensation budget?

Yes. With 14 U.S. states now requiring published salary ranges, your pay bands need to be defensible and documented, not arbitrary. A bottom-up approach tied to market benchmarks makes it much easier to publish ranges you can actually hire within and defend internally.

What is the biggest mistake companies make in compensation budgeting?

Most companies rely only on top-down budgeting. This works initially but breaks when real decisions—like hiring or retention adjustments—don’t fit the budget. The result is reactive changes mid-cycle instead of planned trade-offs early on.

Ready to modernize your workforce and compensation strategy?

See how CandorIQ brings workforce planning and compensation together with AI.