15 Effective Workforce Cost Reduction Strategies for CFOs in the USA

A CFO’s guide to workforce cost reduction strategies: cut payroll spend, uncover hidden costs, and make decisions that hold beyond this quarter.

Workforce cost-reduction strategies are actions companies take to lower payroll and people-related expenses while maintaining business performance. For most CFOs, this is not optional. Workforce spend is often the highest cost on the P&L, and it continues to rise, with U.S. labor costs increasing by about 3.3% year over year in 2025.

The challenge is not finding ways to cut costs. It is choosing the right actions without damaging revenue, productivity, or long-term growth. Quick decisions like hiring freezes or layoffs can reduce spend immediately, but without clear visibility into where costs sit, those savings rarely hold.

This is where cost reduction needs a more deliberate approach. Instead of broad cuts, the focus shifts to aligning workforce spend with business priorities so savings hold beyond the current quarter.

This guide breaks down 15 workforce cost-reduction strategies by timing and risk, so you can act with clarity and avoid reactive decisions that create bigger problems later.

At a Glance

- Workforce cost reduction is most effective when aligned to business priorities, not driven by blanket cuts or short-term pressure.

- Start with immediate levers like hiring controls, contractor audits, and bonus accrual reviews to stabilize spend without structural disruption.

- Sustainable savings come from structural changes such as headcount rightsizing, pay band governance, and tighter approval workflows.

- High-impact actions like furloughs or layoffs should only follow data-backed modeling and clear workforce segmentation.

- Execution succeeds when finance operates with a unified, real-time view of workforce costs and links planning directly to hiring and compensation decisions.

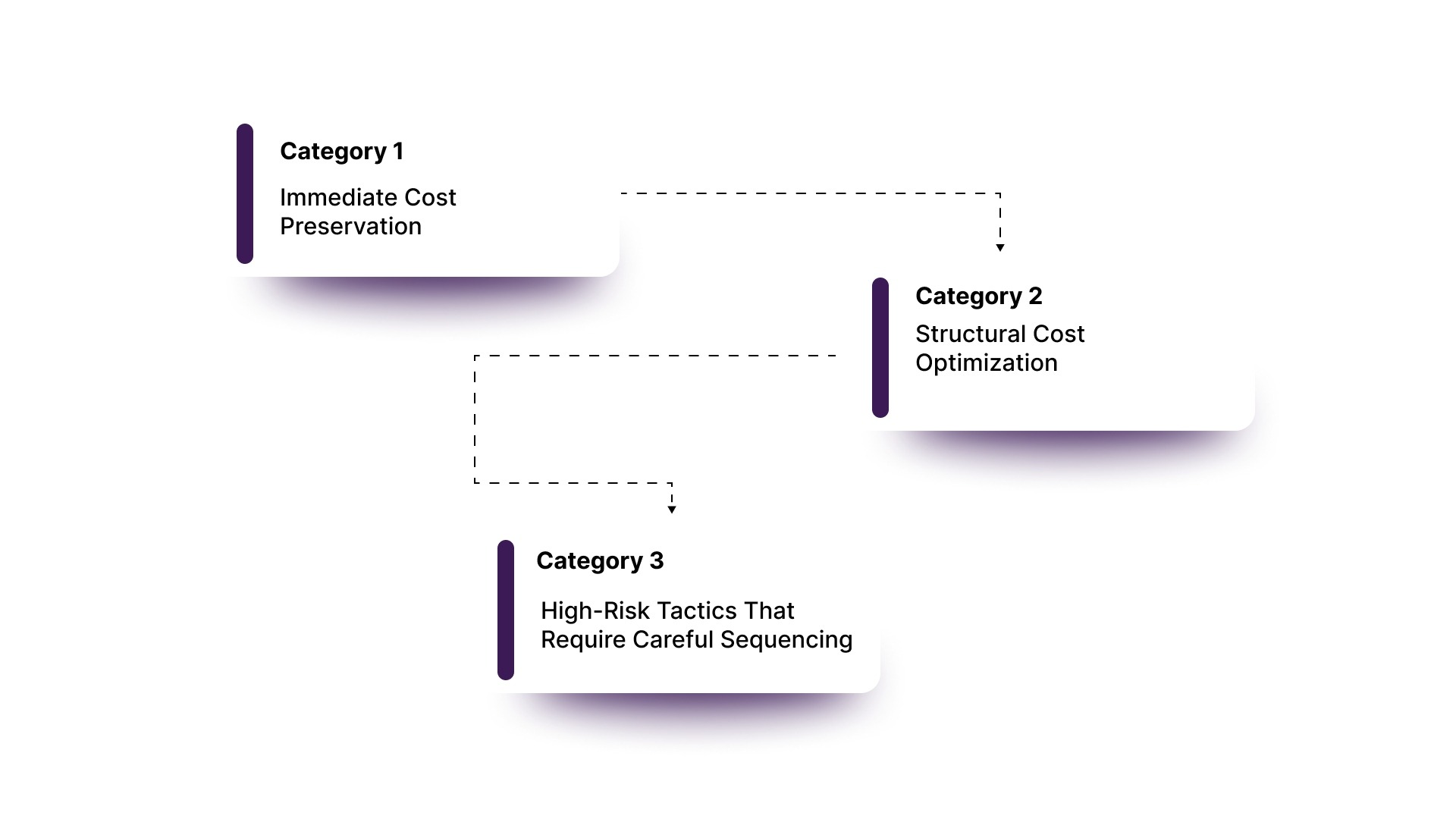

15 Workforce Cost Reduction Strategies (Grouped by Decision Type)

Not every strategy fits every situation. The three categories below help you identify which moves apply based on your timeline, risk tolerance, and where the cost problem is actually sitting.

Category 1: Immediate Cost Preservation (Short-Term, Lower Structural Risk)

Start here when budget pressure is immediate. These moves stop new spending without requiring legal process or permanent headcount changes.

1. Hiring Freeze on Non-Critical Roles

Future demand control: stops new headcount from entering the budget.

Pauses backfills and new approvals for roles not tied to revenue or core operations. No severance cost, no legal process, spend stops before it starts.

How to implement:

- Categorize every open req as revenue-critical, operationally essential, or deferrable.

- Issue a written freeze policy with a defined review date.

- Gate every exception through Finance sign-off. Without it, exceptions become the norm.

- Track the productivity impact of unfilled roles monthly, and know when the freeze costs more than it saves.

Risk to watch: Beyond 90 days without a plan, attrition accelerates as remaining employees absorb the load.

2. Contractor and Contingent Workforce Audit

Hidden spend recovery: finds costs that never appear in headcount reports.

Contractors spend hides across procurement codes, project budgets, and department cards. Companies that have not audited contingent labor in six months routinely find 10-20% tied to completed or paused work.

How to implement:

- Compile a full list from procurement, HR, and department budget holders. Reconcile all three.

- Map each engagement to an active project. Flag anything without a current scope.

- Issue a 30-day wind-down notice for flagged engagements unless a business leader formally reauthorizes.

- Tighten the approval workflow so this audit does not repeat every quarter.

3. Variable Pay and Bonus Accrual Review

Near-term cash lever: frees working capital without touching base salary.

Bonus accruals sit on the balance sheet as a cash liability before payout. Where thresholds have not been met, reducing those accruals mid-year is one of the cleanest short-term moves available.

How to implement:

- Identify which bonus components are contractually guaranteed versus discretionary.

- Review the current-period accrual by department against actual performance versus payout thresholds.

- For accruals tied to unmet thresholds, formally adjust in coordination with your controller.

- Involve employment counsel before reducing anything that could be interpreted as contractually committed.

4. Compensation Freeze or Merit Cycle Delay

Forward cost control: avoids a run rate increase without cutting current pay.

Pausing or narrowing a merit cycle prevents an increase in compensation costs. Unlike a layoff, it requires no severance and no headcount change. The savings are forward-looking; you avoid the increase, not the current cost.

How to implement:

- Identify which populations are covered by contractual merit commitments versus discretionary increases. Contractual ones cannot be paused without legal review.

- If a full freeze is too blunt, limit increases to roles below the market midpoint or top performers only.

- Communicate early with a clear rationale and a specific resume date. Ambiguity drives attrition faster than the freeze itself.

- Model voluntary attrition risk by role before announcing, especially in competitive talent markets.

Risk to watch: Cannot be sustained beyond one cycle without meaningful flight risk on high performers.

5. Offer Letter and Pending Hire Audit

Pipeline control: catches in-flight payroll commitments before they lock in.

When a budget cut hits mid-cycle, the talent pipeline already has offers moving. These commitments are closer to locking in than they appear, and most Finance teams miss them entirely during a budget correction.

How to implement:

- Generate a report of all offers extended but not yet accepted or in progress in your ATS.

- Categorize each pending hire as revenue-critical, operationally essential, or deferrable.

- For deferrable offers, issue a formal deferral notice with a review date. For rescissions, involve legal counsel first.

- Build a pre-offer Finance checkpoint into your recruiting workflow.

Risk to watch: Rescinding offers carries reputational and legal risk by jurisdiction. Legal review before execution is non-negotiable.

Note: A common mistake at this stage is treating the hiring freeze as the complete solution. In most mid-sized US companies, contractor spend, and in-flight bonus accruals represent a larger untapped savings opportunity than pausing open requisitions alone.

Category 2: Structural Cost Optimization (Medium-Term, Higher Planning Requirement)

These change how work is structured, governed, or compensated. More planning is required, but the results hold.

6. Headcount Plan Rightsizing Against Business Priorities

Planning correction: removes or defers headcount approved in a different business environment.

Headcount plans are built when growth assumptions are optimistic. When conditions shift, the plan rarely updates automatically. Rightsizing reconciles approved roles against current targets and removes what no longer fits.

How to implement:

- Map every open role to a current business priority or revenue driver.

- Sort open roles with each business lead: fill now, defer, or remove from plan.

- Calculate payroll savings from deferred and removed roles and update the budget.

- Set a quarterly headcount plan review to keep it current.

Risk to watch: Roles marked as deferred by Roles Finance are often seen as essential by hiring managers. Come with data linking each role to a specific business output.

Workforce cost is not just headcount. It is how compensation is structured, distributed, and governed. The next four strategies address that layer.

7. Role and Compensation Band Rationalization

Payroll run rate control: stops compensation drift before it compounds.

When pay bands are undefined or inconsistently applied, ad hoc offers and exception-based promotions quietly inflate the run rate. Rationalizing bands by role, level, and location stops that drift.

How to implement:

- Review compensation data by role and level. Identify where active pay falls outside bands or where no band exists.

- Benchmark against market data for your industry and geography. Mercer and Radford are standard US references.

- Redesign bands where the gap to the market midpoint is most significant. Document them formally.

- Apply updated bands to all future offers and promotions. Require approval from Finance and HR for exceptions.

8. Location and Remote Work Cost Arbitrage

Structural overpayment fix: aligns remote pay to geography, not headquarters.

Many companies set remote compensation at headquarters rates. For location-agnostic roles, paying San Francisco rates to someone in Austin or Nashville is structural overpayment that compounds with every new hire.

How to implement:

- Identify which roles are location-agnostic and compensated above their local market rate.

- Build a geo-pay policy with defined location tiers and pay adjustments. US HR benchmarking providers publish geographic differential data.

- Apply the policy to new hires going forward. Preserve existing pay and communicate that future increases follow the new policy.

- State the policy clearly during the recruiting process so candidates understand it before receiving an offer.

9. Benefits and Total Compensation Audit

Benefits spend recovery: identifies costs that do not translate into retention or productivity.

Benefits represent approximately 30% of total compensation for US private industry workers, according to the BLS. Most Finance teams review this only at renewal. Underused benefits, wellness stipends, premium perks, and equity refresh schedules are real cost levers that rarely get treated as such.

How to implement:

- Request utilization data for each benefit from your benefits provider or HR platform.

- Identify benefits where the cost per enrolled employee is high, and utilization is low. These are the clearest restructuring candidates.

- Model retention risk by role before removing anything. Some benefits matter more to specific talent segments than utilization rates suggest.

- Sequence changes to your annual renewal window. Mid-cycle changes to health or retirement plans carry legal and notice requirements.

10. Workforce Productivity and Span-of-Control Review

Org overhead reduction: surfaces management layers that consume payroll without adding output.

Fast-growing organizations accumulate management layers quickly. Managers with one or two direct reports, parallel teams doing similar work under different budget owners — this overhead does not appear in a standard headcount report but represents real payroll cost.

How to implement:

- Review your org chart and calculate the manager-to-IC ratio by department. Below 1:5 in most functions is worth investigating.

- Identify managers with fewer than three direct reports. Determine whether the structure reflects genuine complexity or accumulated hierarchy.

- Look for parallel teams in functions like analytics or operations doing similar work under different VP-level owners.

- Model the payroll impact of consolidating redundant layers before making structural changes.

Risk to watch: Structural changes driven by instinct rather than data often remove the wrong layers. Map first, cut second.

11. Headcount Approval Gate Tightening

Governance control: prevents unapproved headcount from being included in the budget in the first place.

In most fast-growth companies, Finance learns about a hire when the offer is already in progress. Tightening the gate means requiring Finance sign-off before any requisition opens in the ATS, not after.

How to implement:

- Map your current headcount request process. If Finance is notified after the request is open, the gate is not working.

- Redesign the workflow so that Finance sign-off, including budget confirmation and role-to-priority mapping, is required before the request is created.

- Introduce a standardized request form with budget line confirmation, business justification, and a proposed start date.

- Run a monthly report showing open requisitions versus approved budget by department so variances surface before they compound.

12. Workforce Segmentation by Cost and Criticality

Decision map: ensures cuts target the right spend, not just the most visible spend.

Before any broad cost reduction, you need a map of where spend is concentrated and which roles drive the most business value. Without it, cuts default to even-handed reductions that preserve low-value spend while eliminating high-value capacity.

How to implement:

- Build a role-level view showing fully loaded compensation cost alongside a business output metric for each function.

- Plot roles on a two-by-two matrix: high cost and high criticality are protected; high cost and low criticality are the primary target.

- Share the segmentation with senior leadership before any reduction is communicated. Alignment prevents execution disputes.

- Use this segmentation to inform every Category 3 decision. No high-risk tactic without it.

Category 3: High-Risk Tactics That Require Careful Sequencing

Only after Categories 1 and 2 have been fully modeled. If structural optimization is not exhausted first, these tactics mask the problem rather than solve it.

13. Voluntary Separation Programs (VSPs)

A structured incentive for employees to leave voluntarily, avoiding the legal and reputational cost of a forced RIF.

A VSP offers eligible employees an enhanced severance package in exchange for voluntary resignation. It is most useful when headcount reduction is necessary, but the risk of a traditional layoff is too high.

How to implement:

- Define eligibility criteria carefully. Overly broad eligibility risks losing high performers. Consider restricting by role type, level, or tenure.

- Design the package with employment counsel. Enhanced severance, continued benefits for a defined period, and COBRA support are standard US components.

- Set a clear acceptance window, typically 30-60 days, with a defined departure date. Open-ended VSPs create planning uncertainty.

- Model the financial impact under best-case, expected, and worst-case participation scenarios before announcing.

Risk to watch: Participation is self-selected. High performers with strong external options are often the first to accept. Design eligibility criteria to limit this and have a retention plan ready for critical talent.

14. Furloughs

A temporary pause in pay or hours that keeps employees in the workforce without triggering termination obligations.

Furloughs reduce payroll costs without severance or the legal process of a termination. They work when the pressure is genuinely temporary: a cyclical revenue dip, a delayed project, or a quarterly gap expected to recover.

How to implement:

- Confirm legal requirements for furloughs in each US state where your employees are located. Wage and hour laws vary significantly by state.

- Define the terms precisely: which employees are affected, the reduction in hours or pay, the duration, and the return-to-full date.

- Communicate clearly and early. Employees with a defined return date are significantly more likely to stay than those facing open-ended ambiguity.

- Set a formal checkpoint at the midpoint to assess whether the business condition is recovering as expected.

Risk to watch: If the pressure is not genuinely temporary, a furlough is a delayed layoff with added administration and morale cost.

15. Targeted Layoffs

Permanent elimination of roles in specific functions or levels when structural savings are confirmed as necessary.

Nearly two-thirds of large US organizations conducted three or more rounds of cost-cutting between 2023 and mid-2025, yet still failed to reduce operating expenses, largely because layoffs were implemented without a full financial model. (Source: Gartner, September 2025.)

How to implement:

- Build a full cost model before announcing. Include direct severance, state unemployment insurance rate impact, productivity loss during transition, and projected backfill cost over 12-18 months.

- Use the workforce segmentation from Strategy 9 to identify which roles to target. Avoid even-handed cuts across departments.

- Confirm WARN Act requirements if the reduction affects 50 or more employees at a single US location within a 30-day window.

- Communicate the decision clearly, at once, with a credible rationale. Staged announcements significantly impact morale and retention.

Risk to watch: High. Direct impact on morale, employer brand, institutional knowledge, and team productivity. This is a last resort, not a first response.

How to Prioritize Workforce Cost Reduction Strategies: A CFO Decision Framework

Before selecting any strategy, three questions should anchor your decision. Getting these right before you act separates sustainable cost reduction from reactive cutting that compounds problems a quarter later.

Question 1: What is the time horizon of the budget pressure?

- Immediately, this quarter: Start with Category 1

- Medium-term, next 6–12 months: Build toward Category 2

- Structural and ongoing: Sequence through Category 2 before considering Category 3

Question 2: Where is the cost actually concentrated?

- Workforce spend rising but headcount flat: Audit contractor spend and variable pay accruals first.

- Headcount growing faster than revenue: Rightsizing the headcount plan is your highest-leverage move.

- Compensation inconsistency across roles: Pay-band rationalization unlocks simultaneous cost and equity improvements.

Question 3: What is your risk tolerance?

- Low: Contractor audits, hiring freeze, pending offer review, headcount approval gate tightening.

- Moderate with medium-term pressure: Structural strategies in Category 2

- Higher tolerance with confirmed structural need: Category 3 only, after full scenario modeling

Use this sequencing guide as your starting point:

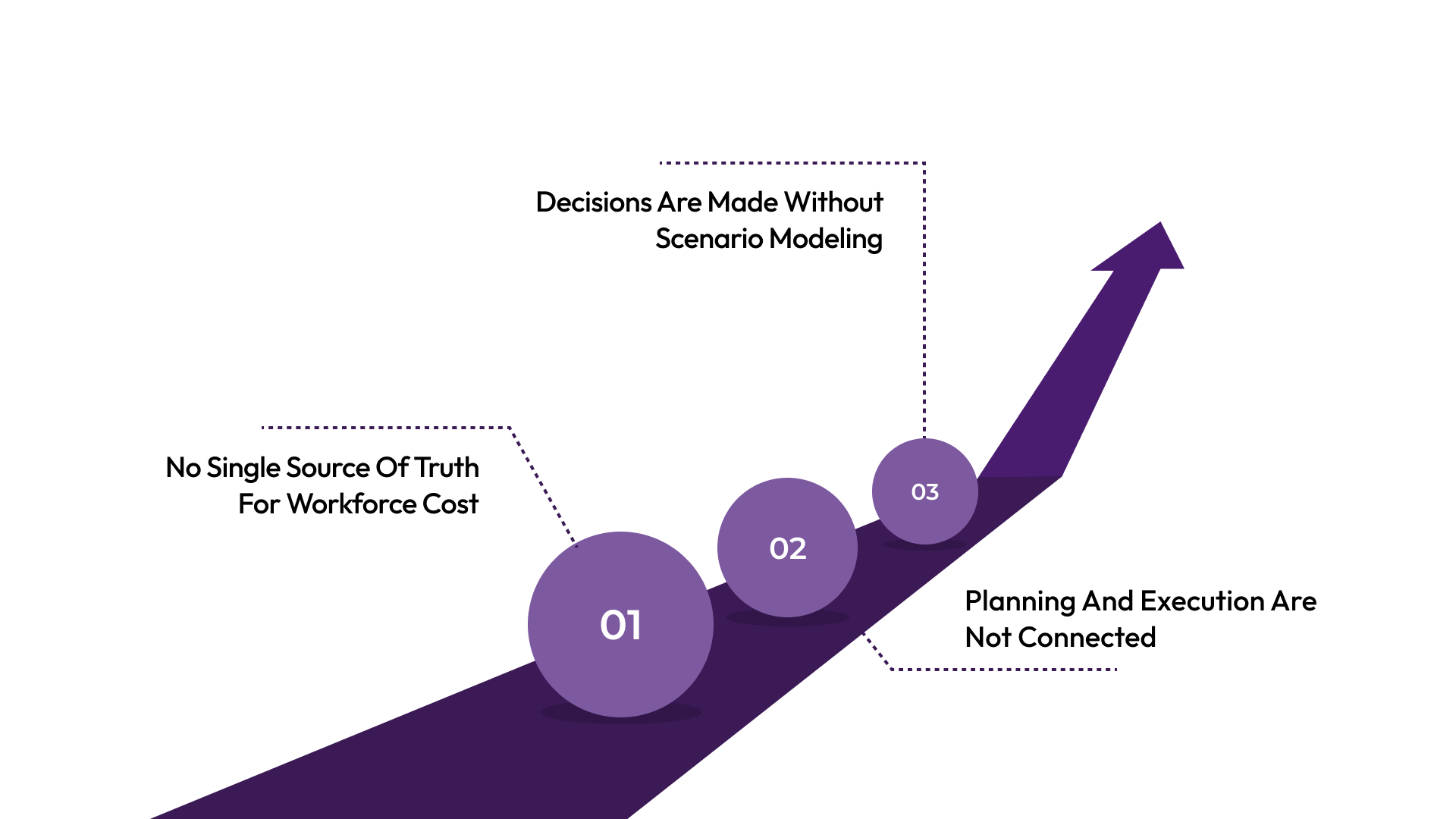

Why Workforce Cost Reduction Plans Fail in Execution

Even with the right strategies and sequencing, many cost reduction plans fail to deliver what was modeled. The issue is not the strategy. It is the gap between how decisions are made and how they are executed.

Three structural breakdowns show up consistently.

Problem 1: No Single Source of Truth for Workforce Cost

Workforce cost data is stored across multiple systems, including payroll, HRIS, planning sheets, and procurement. Each reflects a partial view, but none shows the full picture.

Decisions are made on incomplete visibility. Cost appears to be controlled at the summary level, while imbalances persist beneath. One function may run over budget while the contractor's spending expands beyond headcount, or the planned versus actual figures diverge mid-cycle.

- What fixes it: Operate from a unified, real-time view of workforce spend versus plan, broken down by role, department, and location. Decisions should reflect the current state rather than static reports.

Problem 2: Planning and Execution Are Not Connected

Headcount plans, hiring decisions, and budget approvals often move through separate workflows.

Finance models are cost-based on an approved plan. Execution happens through hiring and compensation decisions that are not consistently tied back to that plan.

Over time, headcount deviates from approved targets, roles are added without clear budget alignment, and timing differences distort actual spend.

- What fixes it: Link headcount requests, compensation decisions, and budget approvals into a single controlled process. Every change to workforce cost should be traceable to an approved plan and reflected immediately in the budget.

Problem 3: Decisions Are Made Without Scenario Modeling

Many cost actions are evaluated only at the point of decision. A hiring freeze, compensation change, or reduction may appear efficient in isolation, but its downstream impact is rarely modeled in full.

Productivity impact is not accounted for, attrition risk is underestimated, and future replacement costs are not included in the decision.

- What fixes it: Evaluate decisions through forward-looking scenario models before execution. Measure not just immediate savings, but total cost impact over time, including productivity and backfill.

Workforce cost reduction is not just about choosing the right lever. It depends on executing decisions on complete, connected, and current data. Without that, even well-planned strategies fail to deliver the expected impact.

How CandorIQ Gives CFOs the Visibility to Act on Workforce Costs?

Every strategy in this guide depends on one thing you may not have right now: a clear, real-time picture of what your workforce is actually costing versus what the plan said it would. CandorIQ is a compensation and headcount planning platform that gives you that picture, so your cost-reduction decisions are based on current data, not last quarter's export from the HRIS.

- Headcount Scenario Planning lets you model the financial impact of hiring freezes, headcount deferrals, and workforce changes before you commit. Compare multiple scenarios against your budget thresholds in real time, so you know the downstream cost of each option before the announcement goes out.

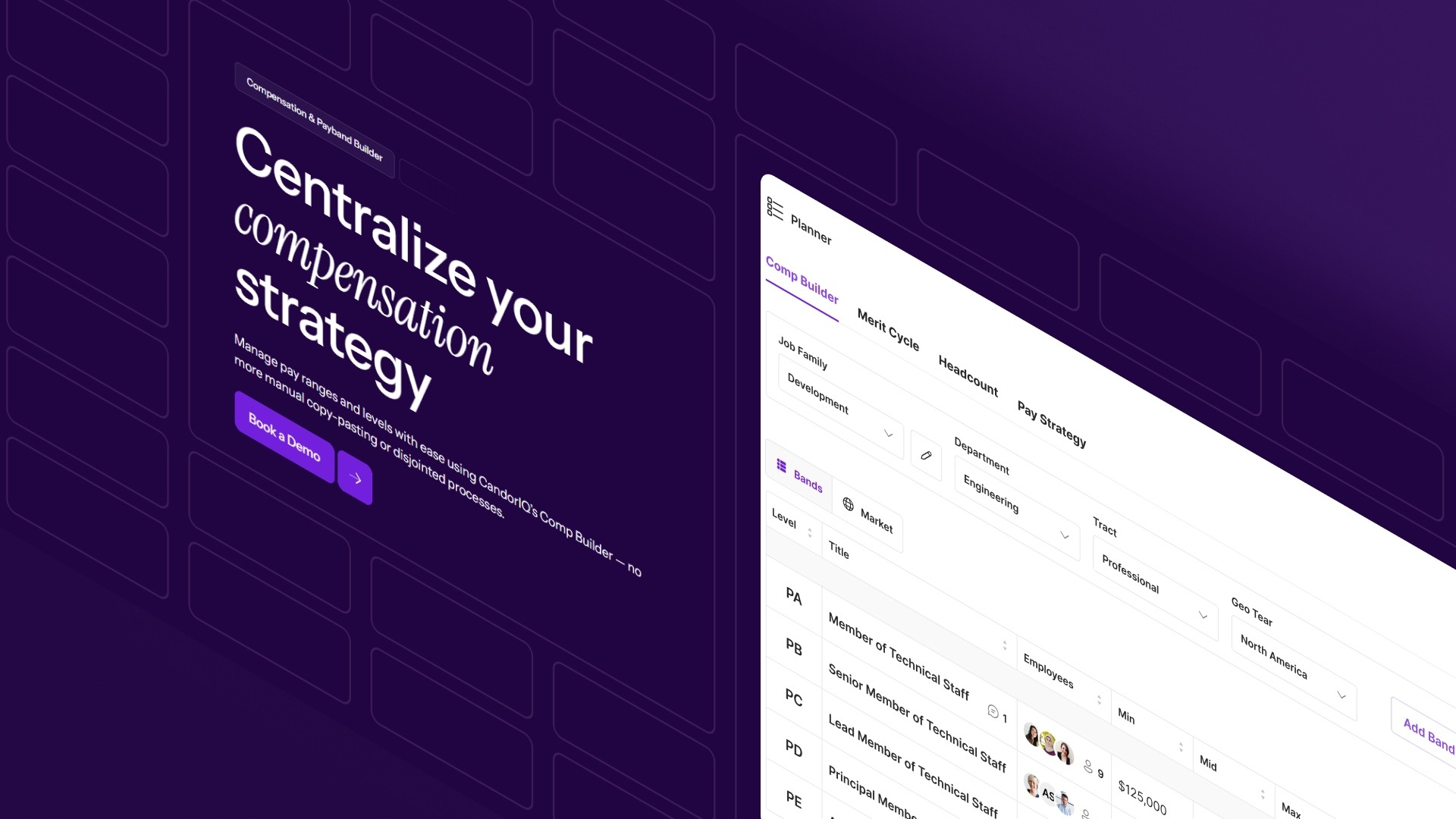

- Compensation and Payband Builder lets you define and enforce pay bands by role, level, and location. Every offer and promotion decision happens inside a defined structure, which stops the compensation drift that quietly inflates your payroll run rate quarter over quarter.

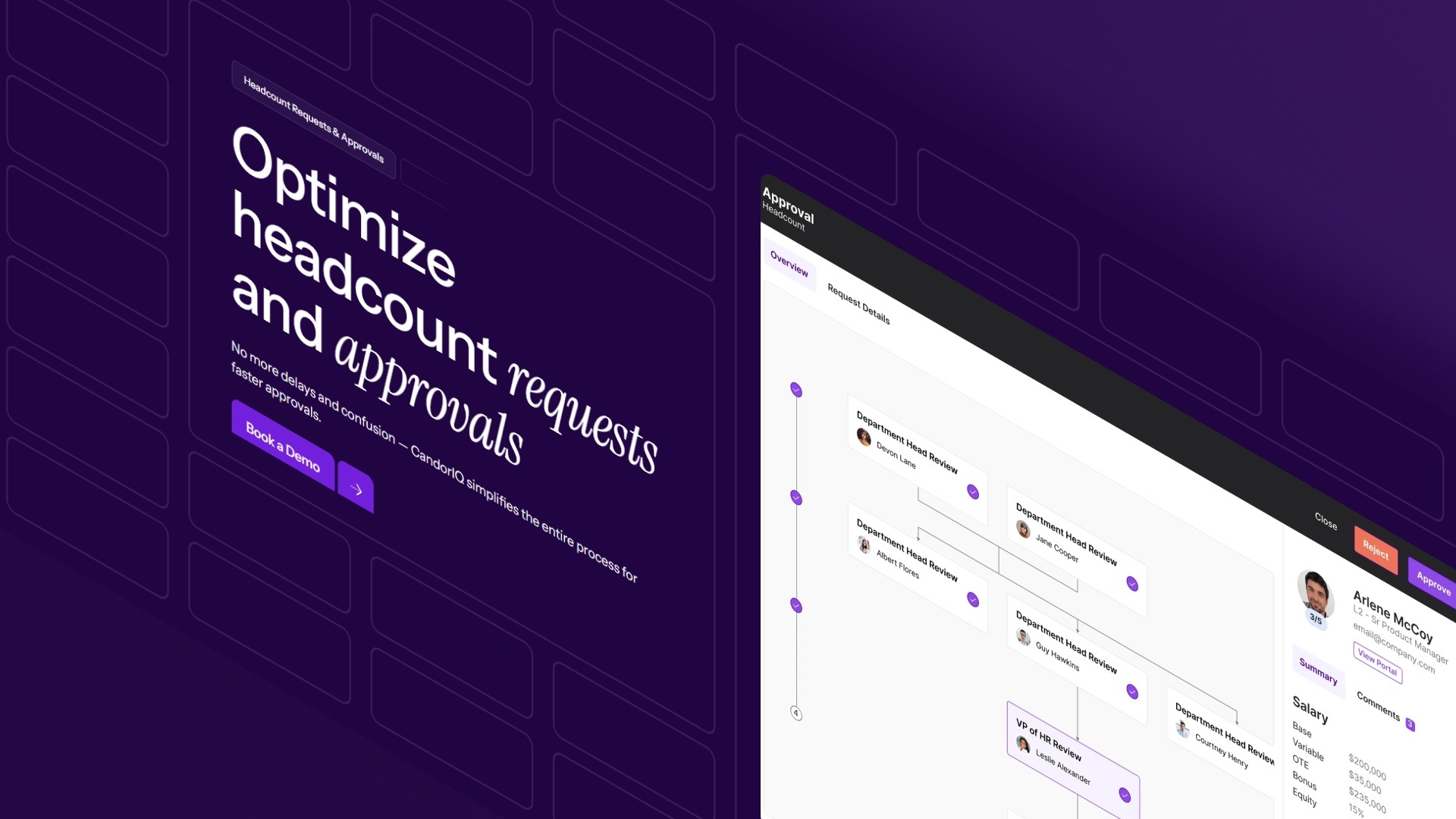

- Headcount Requests and Approvals puts your budget sign-off into the workflow before a requisition opens, not after the offer is already in progress. You get documented business justification and budget confirmation on every new hire request, routed to you automatically.

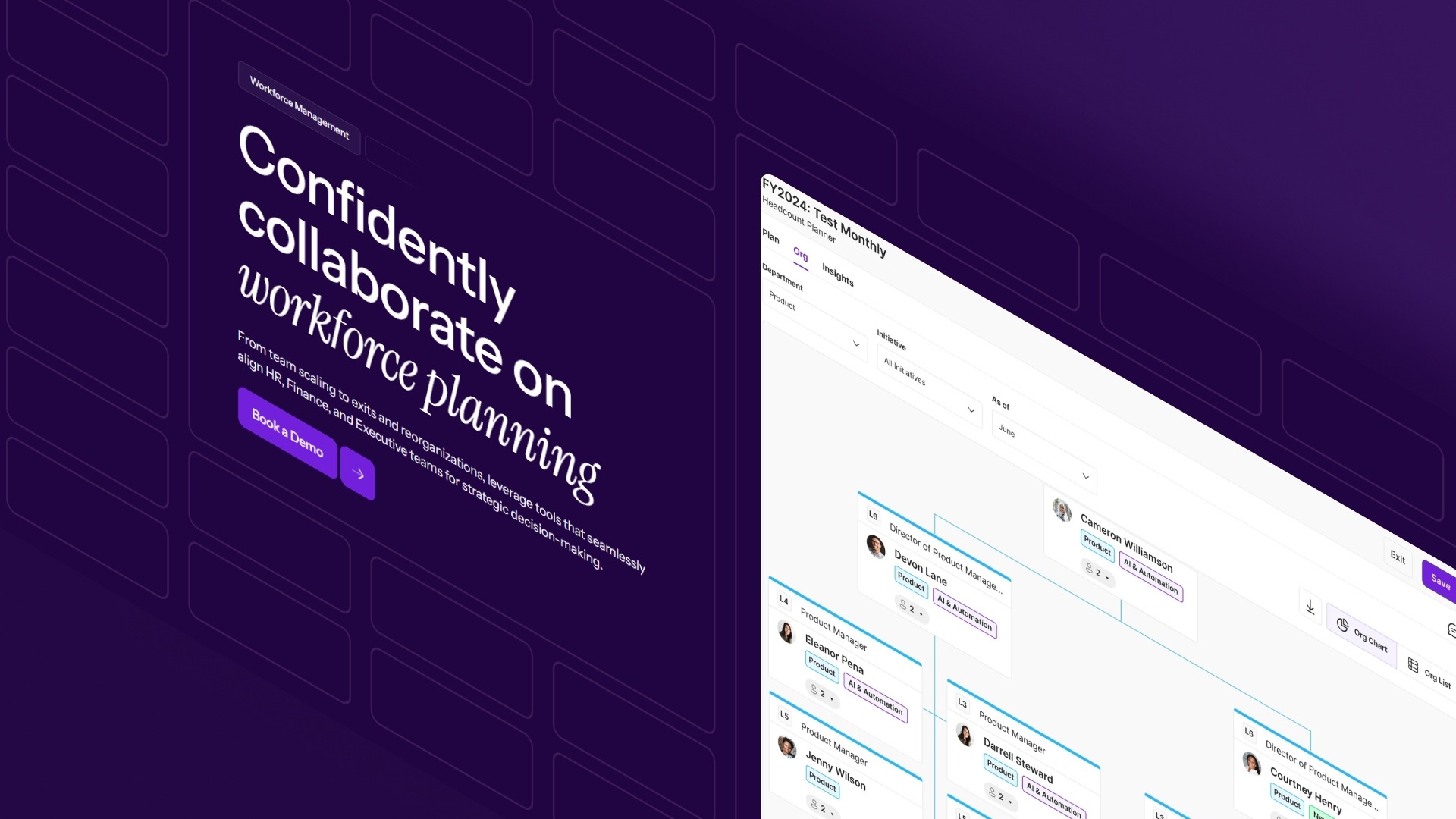

- Workforce Management gives you a single view of actual headcount and compensation spend against plan by department and level. You can see where spending is running ahead in the current period, not at quarter close, when your options are already limited.

Workforce cost-reduction decisions only hold when backed by accurate, real-time data. Without that, even well-planned strategies turn into reactive cuts that miss the real problem.

If you want to see exactly where your workforce costs stand and how different decisions impact your budget before you act, CandorIQ gives you that clarity.

Book a demo now and see how you can plan, model, and control workforce spend with confidence.

.png)

FAQs

1. How do I know which workforce cost reduction strategy to prioritize first?

Start by identifying where costs are concentrated and your time horizon. Immediate pressure calls for hiring controls and audits, while structural issues require headcount rightsizing and compensation governance.

2. What is the biggest mistake CFOs make when reducing workforce costs?

Most CFOs rely on broad cuts like layoffs without full visibility. This often shifts costs elsewhere instead of reducing them, leading to recurring budget gaps and weakened productivity.

3. How can I reduce workforce costs without impacting business performance?

Focus on non-disruptive levers first, like contractor audits, bonus accrual adjustments, and hiring controls. These reduce spending without affecting core operations or long-term growth capacity.

4. When should high-risk actions like layoffs or furloughs be considered?

Only after exhausting short- and medium-term strategies with clear data. High-risk actions should follow workforce segmentation and scenario modeling to avoid damaging critical business functions.

5. Why do workforce cost reduction plans often fail in execution?

Execution fails due to disconnected systems, a lack of real-time data, and no scenario modeling. Without a unified view of workforce costs, decisions don’t translate into sustained financial outcomes.

Ready to modernize your workforce and compensation strategy?

See how CandorIQ brings workforce planning and compensation together with AI.